Money would be much easier to understand if everyone started thinking about 'access into the marketplace'. Especially, it would easier to understand the creation of money.

The essence of the creation of money is the gift of 'assess into the marketplace'. Ownership of money is ownership of tangible evidence that intangible 'access into the market' has been granted.

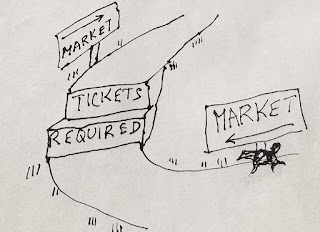

Owning money is like owning a ticket. If we characterized money as a 'ticket', we would intuitively understand that money embodies evidence of intangible 'assess into the marketplace'. Numbers on the ticket would represent the increment of access granted by each ticket.

We can still talk about money as we presently do. Just don't think of money as being debt or an IOU. Think of money as having the characteristics of a ticket which carries within it the intangible of access.